ORLANDO, Fla. — Freshness gets a product considered, but the brand often gets it chosen. That was the central message from Acosta Group during a June 8 session at the IDDBA Show at the Orange County Convention Center, where two company leaders unpacked new research on how shoppers weigh national brands against private label across the fresh perimeter.

In “Rising Together: How Brand and Private Label Synergy Drive Growth in Fresh Prepared Foods,” Kathy Risch, senior vice president of thought leadership and shopper insights, and John DuBois, vice president of fresh foods, U.S., argued that the question facing retailers is not national brand versus private label. It is how to use both, because, as DuBois put it more than once during the presentation, “all tides rise together.”

Inside The Research

The findings come from Acosta Group’s “Fresh Insights: Why Brand in Fresh Requires a Different Lens” study, conducted in March 2026 among 2,226 U.S. shoppers ages 18 to 79 who had purchased fresh bread, shredded cheese, refrigerated salsa or refrigerated pasta within the prior three months. Roughly 250 shoppers evaluated each product concept. Respondents were drawn from the company’s proprietary Shopper Community of more than 40,000 demographically diverse U.S. household shoppers.

Risch said the team deliberately went narrow rather than wide, concentrating on four highly shopped dairy, deli and bakery categories so it could measure how brand behaves when shoppers face real trade-offs.

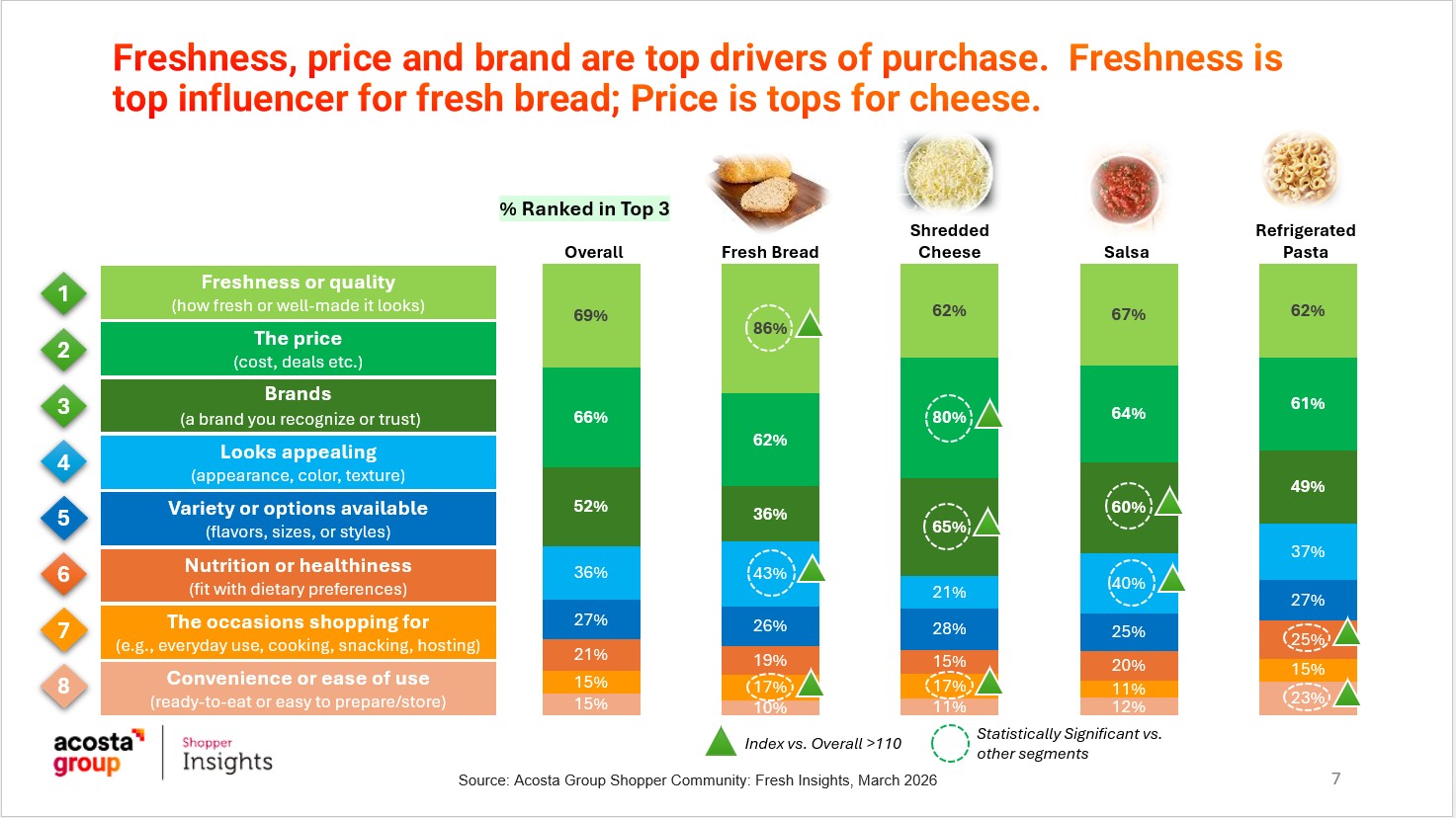

Freshness And Price Lead, But Brand Shapes The Choice

When shoppers were asked what matters most in fresh, freshness or quality ranked first at 69 percent, followed by price at 66 percent and brands at 52 percent. Those fundamentals set the baseline, Risch said, but brand becomes a more powerful factor the moment shoppers are forced to choose between comparable options, especially in categories where quality is harder to judge by sight.

The pull of national brands showed up clearly in forced-choice testing. Across the four categories, shoppers preferred national brand concepts 61 percent of the time over store brand concepts. National brands also carried a 17 percent higher “fair price” perception overall, with shoppers pegging a fair price at $5.90 for national brand concepts versus $5.03 for store brands.

Risch also noted that shoppers want national brands present in the perimeter. In the research, 82 percent said it is important that the fresh area of the store include well-known, nationally advertised brands, a signal that assortment, not just price, drives how shoppers judge the section.

Value Varies By Category, Shopper And Occasion

The impact of brand was far from uniform. Refrigerated pasta emerged as one of the most brand-influenced categories, with national brands outperforming on appeal, trust and preference. Cheese showed the widest price gap, with shoppers expecting roughly a 32 percent higher price for the national brand. Salsa told a different story: shoppers rated store and national brands similarly on quality and appeal, yet still reached for the national brand more often at the final moment of decision.

Generation mattered, too. Millennials and Gen Z showed the greatest willingness to pay a premium for national brands in fresh. Gen Z assigned national brands a 21 percent higher fair price than store brands, the largest gap of any generation studied.

Acosta Group’s segmentation found that national brand seekers made up the largest group at 44 percent of fresh shoppers, followed by occasion-driven explorers at 30 percent and private label loyalists at 22 percent, alongside a convenience-first practical segment. One of the study’s most striking findings, Risch said, was that even private label loyalists assigned national brands a higher fair price for certain fresh occasions, underscoring the difference between an everyday default purchase and a higher-confidence occasion buy.

A Halo Effect Across The Department

The research also pointed to a halo effect when the two brand types sit side by side. Most shoppers said that seeing a familiar national brand alongside a store brand made the section feel more trustworthy, rather than diminishing the store brand. In the concept testing, the national brands shown included names such as La Brea Bakery in artisan bread, BelGioioso in cheese, Buitoni and Rana in refrigerated pasta, and Sabra in dips and salsa, each paired against a generic store brand equivalent.

DuBois said national brands expand reach and bring new shoppers into a category, while behaving like higher-value buyers once they choose, purchasing more frequently and at higher units per trip. Store brands, he said, remain essential anchors for everyday value, margin efficiency and loyalty among price-focused shoppers.

All Tides Rise Together

In an announcement accompanying the research, Mark Rahiya, group president of omnichannel sales and services, said the strongest fresh strategies leverage both brand types. Store brands anchor value and everyday loyalty, he said, while national brands expand category reach, strengthen trust and attract incremental, higher-value shoppers.

DuBois closed on the same note, telling the audience the takeaway is not that one brand type is better than the other. “Ultimately, all tides rise together,” he said.

More detail on the study is available through Acosta Group at acosta.group/how-fresh-foods-are-rewriting-the-rules-of-brand-loyalty.