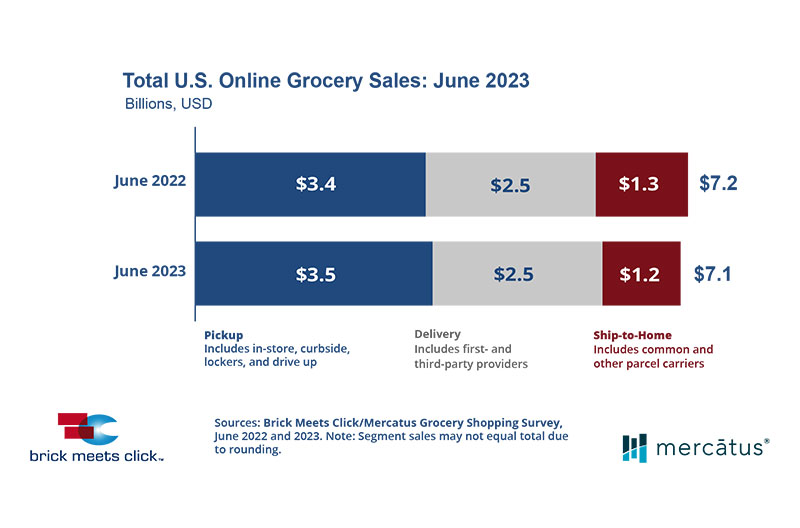

The U.S. online grocery market finished June with $7.1 billion in total sales, down 1.2 percent compared to last year’s $7.2 billion, according to the latest monthly Brick Meets Click/Mercatus Grocery Shopping Survey.

Although more households bought groceries online in June than last year, these users completed fewer orders during the month and average order values had mixed results across the segments.

The number of monthly active users buying groceries online expanded by more than 1 percent in June and the overall average order value rose 3 percent versus a year ago. However, neither of these gains was great enough to offset the more than 5 percent drop in the average number of orders completed during the month.

In addition, 70 percent of monthly active users chose to use just one of the three fulfillment methods to receive their online grocery orders, up over 200 basis points compared to the prior year. Pickup’s penetration rose 140 basis points to 56 percent while ship-to-home’s fell 390 basis points to 41 percent and delivery dipped 250 basis points to 39 percent.

Looking deeper into each segment’s performance reveals some trends compared to last month:

- Pickup, much like last month, continued to buck the downward trend experienced by the other two segments. In June, pickup sales grew 3.2 percent versus a year ago and accounted for nearly 49 percent of all eGrocery sales, up 200 basis points from last year.

- Delivery dipped for the second straight month. The segment’s sales declined 2.5 percent compared to June last year, causing its sales share to fall by 50 basis points to just under 35 percent.

- Ship-to-Home continues to face headwinds as U.S. households continue to shift how they receive online grocery purchases. The segment experienced a 9.7 percent drop in sales compared to June last year, capturing just under 17 percent of all eGrocery purchases during the month, a drop of 150 basis points versus a year ago.

- The overall repeat intent rate was flat at 63 percent versus a year ago, ending the three-month slide reported from March through May. The current overall rate still lags pre-COVID intent rates by more than 10 percentage points, illustrating the challenge that grocers face relative to retaining customers.

“To elevate customer engagement, regional grocers need to improve the perceived value associated with the online shopping experience,” said Sylvain Perrier, president and CEO of Mercatus.

“To achieve this, grocers can focus their efforts on areas like leveraging personalized recommendation algorithms to provide more relevant product suggestions based on individual preferences and past purchases, optimizing the platform’s usability to reduce points of friction and offering personalized discounts, digital coupons and loyalty rewards.”

Online’s share of total grocery spending declined in June, dropping 230 basis points to 11.9 percent versus last year. Excluding ship-to-home, the adjusted contribution from pickup and delivery finished at 10 percent, down 160 basis points compared to a year ago. This was due to delivery’s weaker performance for the month.

For the first six months of 2023, total eGrocery sales were down 1.8 percent versus the same period in 2022. Throughout the first half of the year, pickup continued to win the largest share of sales, gaining 140 basis points over the 2022 period and capturing 47.1 percent of total eGrocery sales.

“Our five-year forecast anticipated that 2023 would be a challenging year for eGrocery, so these results generally align with our expectations,” said David Bishop, partner at Brick Meets Click.

“While ship-to-home declines and delivery have mixed results, pickup’s stronger performance isn’t surprising as it is becoming more widely available and helps customers who want to shop online save money, which is certainly helpful in the current market.”

Study: Regional Grocers Face Mounting Online Competition From Walmart