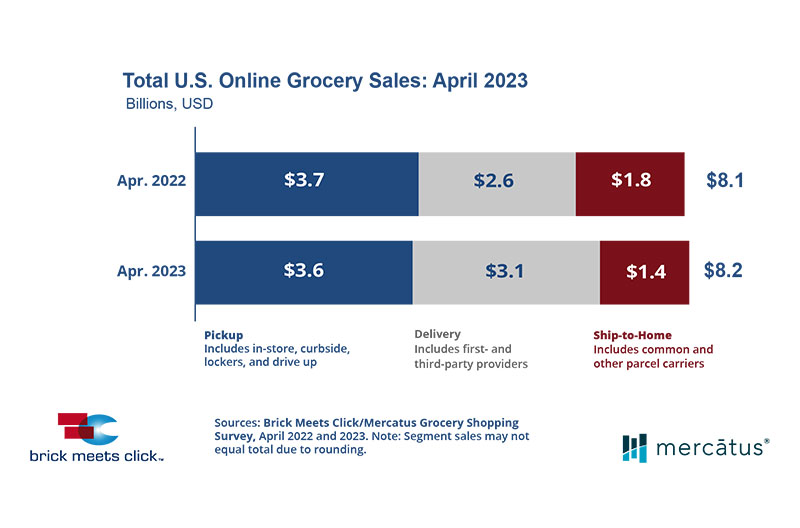

According to the latest Brick Meets Click/Mercatus Grocery Shopping Survey fielded April 28-29, overall eGrocery sales for April totaled $8.2 billion, up 0.9 percent versus a year ago. Year-over-year performance varied across the three key segments as delivery sales jumped 20 percent, pickup dipped 3 percent and ship-to-home plunged 19 percent.

The strong gains for delivery during April were driven by a rebound in monthly active users and a higher average order value. Delivery’s MAU base grew 11 percent versus the prior year but finished up only 1 percent on a two-year stacked basis versus 2021 as the segment’s customer base fell 9 percent last year.

Over the past several years, the expansion of new delivery providers and service offerings has attracted additional customers by making it a more available and attractive way to shop, depending on the mission or occasion. In addition, delivery’s AOV rose about 5 percent on a year-over-year basis while the other two segments experienced a pullback in spending per order versus 2022.

April’s decline in pickup sales was the result of lower order frequency and a reduced AOV; this was offset somewhat by moderate growth in its MAU base (in the mid-single digit range). The decline for ship-to-home sales, on the other hand, was the result of a deterioration across all key shopping metrics, including continued contraction of its MAU base along with double-digit drops in both AOV and order frequency among active users.

“A macro view of the eGrocery market can reveal certain opportunity gaps, but it may also obscure key shopping dynamics within a particular segment of the market,” said David Bishop, partner at Brick Meets Click.

“For example, it’s difficult to see how little overlap exists between the households that use pickup and those that use delivery services or to know that pickup grew stronger in mass during April unless you’re able to dig deeper into the segment dynamics as we do in our monthly reports.”

Repeat intent scores also trended down in April for two reasons that should be particularly concerning for grocery operators. First, the likelihood that a customer will use the same service within the next 30 days for April dropped 530 basis points compared to last year, landing at under 58 percent, driven by a dramatic drop from the most-frequent customers (those who completed four or more orders with a service within the past three months).

Second, the repeat intent rate for mass declined nearly 300 basis points in April versus the prior year, but the repeat intent rate for grocery fell almost 900 basis points, leading to the largest gap recorded to date between the two formats and surpassing the record gap set in January.

Looking at repeat intent rates by receiving method reveals more concerning news for grocers. Grocery’s repeat intent rate for delivery orders has not only declined more than its rate for pickup orders, but it has also dropped dramatically compared to mass delivery services.

This decline, combined with the fact that delivery represents a higher share of online orders for grocery than mass, highlights the importance of controlling the quality of the customer experience. However, ensuring a good experience is often more challenging with delivery orders than for pickup because the distribution function is generally outsourced to a third-party provider.

“Given that customers vote with their wallet, the expanding gap in repeat intent between mass and grocery should be a red flag that warrants grocers re-evaluate all aspects of the customer experience,” said Sylvain Perrier, president and CEO, Mercatus.

“Customers’ expectations continue to evolve based on past experiences, which means it’s vital that grocers continue to improve the execution of various aspects, whether that’s a more personalized experience, fewer out-of-stocks or shortened wait times.”

Total eGrocery spending slid in April, falling 20 basis points to 12.1 percent versus last year. Excluding ship-to-home, since most conventional supermarkets don’t offer it, the adjusted contribution from pickup and delivery finished at 10 percent, up 40 basis points compared to a year ago, due to delivery’s strong performance for the month.

To further analyze current shopping behaviors, the April research wave asked where households bought groceries during the past month. For those households indicating mass, 69 percent reported online grocery activity in April, and for those specifying grocery (excluding hard discount), 54 percent reported online grocery activity.

As to where households bought groceries online, 73 percent of the households that mainly shopped with mass also ordered online from a mass service compared to 52 percent of those identifying grocery as their primary store who also ordered from a grocery service. “These early findings, and others, suggest that winning online goes beyond simply competing online, which future research will examine,” Bishop said.

For additional insights and information about the full report, visit the Brick Meets Click eGrocery Dashboard for April or the eMarket/eShopper page.