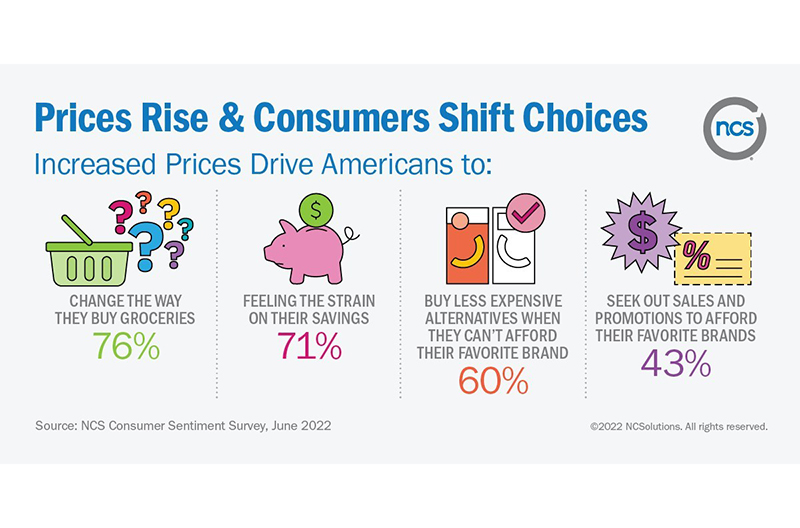

Nearly half of Americans feel like they can’t afford their previous lifestyle and 76 percent of American consumers say their family has changed how they buy food with prices on the rise. In addition, two-thirds are more mindful of how they are spending their money. These findings are part of a new consumer sentiment survey on grocery inflation commissioned by NCSolutions, the leading company for improving advertising effectiveness.

Eighty-five percent of Americans are very concerned or extremely concerned about inflation and almost unanimously (93 percent) they said we’re in an inflationary time. On the same economic theme, 57 percent are concerned about the country’s financial situation, while 47 percent say they’re concerned about their family’s financial situation.

Eight out of 10 Americans expect the cost of living will become somewhat more or much more expensive in the coming year. Sixty-five percent of Americans agree with the statement ‘my income has not increased as fast at the cost of food, beverage and personal care products.’

“For the second time in a little over two years, consumers are pivoting to new purchasing behaviors at the grocery store,” said Alan Miles, CEO, NCSolutions. “Since the start of the pandemic, they’ve been swapping their favorite brands for what’s available. Today, though, value is the centerpiece more often than availability, consumers are selecting brands and products to stretch their budgets as far as possible. CPG brands that meet customers where they are both in this inflationary moment and as prices ease have the best shot at keeping them for the long-term.”

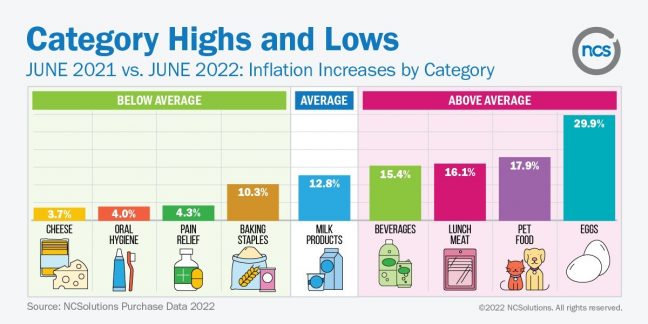

NCSolutions’ proprietary purchase data, which reflects the buying trends of consumers for CPG products, shows an almost 13 percent price increase on average. In a six-year price trend analysis, we see that grocery price increases in 2022 are pacing at an accelerated rate compared to other years. The survey findings bear this out with 58 percent of consumers believing the cost of living will be much more expensive in the coming year and 71 percent feeling the U.S. economy is declining.

On a consumer packaged goods category level, there are wide variations in percentage increases.

Compared to one year ago, six in 10 Americans believe CPG product packaging has gotten smaller but costs the same. Consumers still feel the strain of supply chain issues as 69 percent say there are fewer items of the same product on the shelves. Thirty-six percent of Americans said there is less variety of brands available on the shelf today compared with one year ago.

Over half of American consumers say they find basic food staples more expensive; 40 percent believe a recession will occur in 2023. For almost half of consumers, this means buying fewer non-essential items in the grocery store, or for 43 percent, it means buying only the essentials.

Seventy-one percent of Americans say the increase in grocery prices is straining their savings. For other American consumers, increased prices on the grocery aisle mean seeking out less expensive brands. Other ways consumers are coping with the increased price of groceries are loading up the pantry, freezer or shopping closer to home.

When it comes to consumers’ preferred brands, they have to make tough choices in the grocery store. Sixty percent of consumers seek less expensive alternatives when their favorite brands reach a price beyond their budget. Forty-six percent of consumers plan to go without their favorite brands, and 43 percent of consumers look for sales to offset the cost. In the survey, respondents could select multiple ways they react.

“Though it may be tempting to pull back on advertising, a more effective strategy is to recognize and respond to consumer ‘stress-flation.’ Brands have an opportunity now to build loyalty and attract new customers with empathetic marketing,” said Leslie Wood, chief research officer, NCSolutions. “We’re heading into a period of heavy CPG purchasing moments, such as back to school and the approaching holidays. Compelling, well-targeted advertising is a proven strategy for increasing brand equity and sales both in the short- and long-term.”

The online survey of 2,141 respondents was fielded from June 17-20. Responses presented in this survey were weighted by location, education, income and other demographics to be representative of the overall population.

To read more about the findings, you can download the full report here.