by Anne-Marie Roerink/president, 210 Analytics

Food sales remained very strong the last full week of April. Free of the effects of Easter this year or last, the week ending April 26 provided a glimpse at the elevated everyday demand as a result of more meals having moved to at-home.

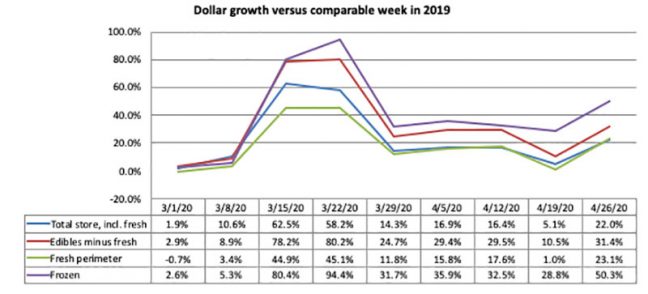

At the same time, the shift to fewer but bigger trips continued and up-ended patterns in terms of day of the week, day part, online ordering, brand and product choices remained. Since the onset of coronavirus in the U.S., the frozen food department has been a sales powerhouse as shoppers looked to stock up and have access to healthy and convenient solutions. 210 Analytics, IRI and AFFI partnered to understand the effect for frozen food in dollars and volume throughout the pandemic.

Rather than showing any signs of slowing, frozen food sales during the week ending April 26 saw their highest increase over the same week last year since March 22, at +50.3 percent. The only department that came close to that was meat, up 49.7 percent. However, decreases in the deli and bakery department pulled down the overall perimeter performance to just over +23 percent. Center store edibles increased 31.4 percent.

Source: IRI, Total US, MULO, 1 week view % change vs. year ago.

Frozen foods generated more than $1.3 billion in the week of April 26, 2020—over $442 million more than the comparable week in 2019. Frozen food unit sales were up 35.8 percent. The highly elevated consumer demand drove continued out-of-stocks at some stores.

On the Retail Feedback Group’s Constant Customer Feedback (CCF) program, a shopper said, “Lots of frozen vegetables were still empty. The selection was OK, but certainly not like normal. More hoarding, I guess.”

The consumer media coverage on the meat supply also resulted in another run on meat, starting the week of April 26. A shopper wrote, “I primarily went for frozen bags of chicken tenderloins and wings, but they were not available.”

On the fresh meat side, some retailers are once more implementing item limits on meat and poultry to stretch supply. Some retailers are also stocking up on more frozen meats to supplement the tight supply in fresh.

“Based on the current market changes as well as announced plant closures, sourcing has been challenging to say the least,” said Samer Rahman, senior director of meat and seafood for Allegiance Retail Services. “With the news reports on plant closures, customers are under the impression meat will not be available in any form. They were alarmed by these reports and started loading up on fresh and frozen meats. The ability to rebound on product in the upcoming weeks is not likely. The demand is too high with limited product supply. I have had to explore additional options, from Australian meats to frozen chicken and burgers to have as an alternate offering to fresh the next few weeks.”

IRI sales data shows that frozen meat, poultry and seafood increased 68.0 percent over the week ending April 26 versus the comparable week in 2019—its highest performance since the week of March 15.

A deep-dive into frozen food sales

The 68 percent gain in frozen meat, poultry and seafood was also the highest of the larger frozen categories. This translated into $415 million in animal protein sales for frozen food the week of April 26, an additional $122 million versus the same week last year. The largest share within frozen foods, frozen meals, increased more than 37 percent. This was driven by continued appetite for frozen pizza, that was up 53.0 percent over the week ending April 26 versus the comparable week in 2019. Frozen snacks also continued to do well, up 76.0 percent.

| Product and share of frozen food department sales for week ending 4-26-20 | % Dollar sales change vs. comparable week ending in 2019 | ||||||||

| 4-26-20 | 4-19-20 | 4-12-20 | 4-5-20 | 3-29-20 | 3-22-20 | 3-15-20 | 3-08-20 | 3-01-20 | |

| Frozen Dept (ex Poultry) | +50.3% | +28.8% | +32.5% | +35.9% | +31.7% | +94.4% | +80.4% | +5.3% | +2.6% |

| Frozen meals (34%) | +37.2% | +27.7% | +21.5% | +27.8% | +25.4% | +99.3% | +88.6% | +3.3% | -2.5% |

| Breakfast food | +42.7% | +30.2% | +22.2% | +25.4% | +21.3% | +81.9% | +72.6% | +4.5% | +1.1% |

| Dinners/entrees | +26.3% | +16.9% | +8.9% | +14.3% | +21.3% | +83.2% | +79.4% | +3.5% | -3.4% |

| Pizza | +53.0% | +51.1% | +47.0% | +58.8% | +53.8% | +143.0% | +120.1% | +3.8% | -2.0% |

| Frozen meat/poultry /seafood (32%) |

+68.0% | +41.5% | +39.2% | +43.0% | +44.7% | +123.1% | +97.5% | +3.5% | +8.3% |

| Processed poultry | +68.3% | +50.6% | +33.7% | +42.6% | +43.7% | +134.7% | +115.8% | +9.2% | +4.3% |

| Meat | +65.1% | +50.0% | +51.8% | +58.5% | +56.9% | +163.6% | +131.6% | +17.9% | +11.0% |

| Seafood | +75.7% | +31.9% | +40.4% | +35.5% | +33.8% | +96.8% | +67.4% | -5.7% | +16.9% |

| Frozen desserts (23%) | +45.9% | +20.8% | +28.6% | +32.0% | +23.9% | +43.1% | +35.9% | +9.3% | +2.2% |

| Ice cream/sherbet | +48.7% | +24.1% | +31.1% | +35.0% | +26.9% | +45.4% | +36.5% | +8.2% | -0.2% |

| Novelties | +44.6% | +25.7% | +21.5% | +27.9% | +20.5% | +40.6% | +36.7% | +11.4% | +6.1% |

| Desserts/toppings | +29.4% | -22.0% | +57.2% | +31.3% | +17.1% | +36.9% | +25.5% | +5.4% | +0.2% |

| Frozen fruits & vegetables (12%) |

+57.6% | +28.7% | +44.6% | +47.4% | +40.7% | +111.4% | +106.7% | +11.8% | +4.3% |

| Fruit | +65.0% | +35.7% | +43.7% | +42.9% | +37.0% | +95.4% | +103.5% | +19.1% | +10.1% |

| Potatoes/onions | +72.7% | +37.8% | +54.4% | +60.7% | +50.1% | +117.3% | +98.3% | +9.0% | +3.2% |

| Plain vegetables | +48.4% | +22.8% | +39.5% | +42.2% | +37.5% | +115.9% | +119.3% | +13.3% | +4.6% |

| Prepared vegetables | +16.9% | -2.4% | +12.8% | +18.4% | +8.8% | +84.5% | +62.9% | -12.6% | -13.4% |

| Frozen baked goods (3%) | +44.0% | -6.9% | +63.2% | +42.4% | +38.9% | +87.8% | +56.8% | +1.4% | -0.8% |

| Frozen snacks (4%) | +76.0% | +58.6% | +49.7% | +56.8% | +46.0% | +127.2% | +97.2% | +4.2% | +1.2% |

| Appetizers/snack rolls | +76.0% | +58.9% | +49.9% | +56.9% | +46.1% | +127.4% | +97.5% | +4.2% | +1.3% |

| Frozen beverages <1% | +65.4% | +41.9% | +63.2% | +62.9% | +59.5% | +142.9% | +114.5% | +8.2% | -1.8% |

| Juices | +65.6% | +42.2% | +63.7% | +63.2% | +59.7% | +143.2% | +114.7% | +8.3% | -1.8% |

Source: IRI, Total US, MULO, 1 week view % change vs. year ago.

Dollars versus units

The slightly longer four-week look shows strong gains for both dollars and units across all areas of frozen. In most areas, dollar sales gains exceed unit sales by more than 10 percentage points. This typically points to consumers opting for larger pack sizes that have a higher per unit cost. It could also indicate some inflationary pressure.

| Category with % of frozen department sales | % sales change over the four weeks ending 4/26/20 versus year ago | |

| Dollar sales | Unit sales | |

| Frozen Dept (ex Poultry) | +36.6% | +25.3% |

| Frozen meals (34%) | +28.3% | +17.9% |

| Breakfast food | +29.6% | +21.3% |

| Dinners/entrees | +16.2% | +6.6% |

| Pizza | +52.6% | +40.3% |

| Frozen meat/poultry/seafood (32%) | +47.3% | +36.4% |

| Processed poultry | +47.9% | +36.1% |

| Meat | +56.2% | +44.7% |

| Seafood | +44.7% | +34.4% |

| Frozen desserts (23%) | +31.7% | +21.1% |

| Ice cream/sherbet | +34.5% | +24.3% |

| Novelties | +29.9% | +21.2% |

| Desserts/toppings | +18.1% | +3.4% |

| Frozen fruits & vegetables (12%) | +44.2% | +33.6% |

| Fruit | +46.4% | +36.3% |

| Potatoes/onions | +55.5% | +50.6% |

| Plain vegetables | +38.1% | +27.7% |

| Prepared vegetables | +11.1% | +4.1% |

| Frozen baked goods (3%) | +31.4% | +28.3% |

| Frozen snacks (4%) | +59.9% | +49.1% |

| Appetizers/snack rolls | +60.0% | +49.1% |

| Frozen beverages <1% | +57.9% | +46.7% |

| Juices | +58.2% | +46.9% |

What’s next?

Going into May, several states have released detailed plans for re-opening in phases. In some, restaurants could reopen starting May 1, though often with social distancing and occupancy rate restrictions in place. The reopening of restaurants in these states may provide an indicator of consumers’ mental readiness and economic ability to re-engage with foodservice. The widely covered meat shortages in consumer media caused another surge in meat demand, both fresh and frozen the first week of May, which likely means highly elevated numbers in next week’s results as well. For the foreseeable future, it is likely that grocery retailing will continue to capture an above-average share of the food dollar.

It is important to remember that the sales surges at retail are only possible thanks to the heroic work of the entire grocery and frozen food supply chains. 210 Analytics and IRI will continue to provide weekly updates as sales trends develop.